Hi, this is tax attorney Anthony Parent, and in this video, I am going to be talking about what the FBAR late filing penalties are. So, what are the FBAR late filing penalties? It's a trick question. There are none. The reason why is because the FBAR comes under different legislation than the tax code. The tax code comes under title 22, title 26, and title 26 authorizes the IRS to charge late filing fees for people who file their tax returns late and if they have a balance due. But the FBAR, everything related to the FBAR, comes from title 31, and that has to do with the Bank Secrecy Act. Now, if you look at title 31, there is no late filing penalty for the FBAR. There's actually something much worse. There is simply a non-filing FBAR penalty, meaning you didn't file one at all. The process is a little bit complicated for the IRS to assess, and typically it would happen during an audit situation where an IRS examiner would conduct two separate audits at the same time. One is for that income tax liability that title 26, and the other is for your FBAR penalties that title 31. Your FBAR penalty would be dependent on whether or not you were willful, which could be up to fifty percent of the account value, or non-willful, which would be ten thousand dollars per occurrence. Now, if you have just a late filing, if you have one late filed FBAR, it's probably not much of an issue. However, if you have many years of FBARs that were never filed, you just don't want to go ahead and file them. What you would want to do in order to reduce your criminal exposure, which is really there, or any significant FBAR penalties,...

Award-winning PDF software

Offshore penalty Form: What You Should Know

Penalties for Reporting U.S. Persons With Respect to Foreign Financial Assets and Accounts — Treasury Jul 18, 2024 — The IRS is also seeking voluntary self-certification that the person is U.S. source to reduce the penalties. In order to do so, information, including but not limited to information related to a foreign source, as required by 26 U.S.C. 6662(i), 6662(h) or 6662a(h)/ The following table summarizes the penalties assessed for violations of foreign reporting requirements under title 26, U.S.C., section 6662. Date of compliance Date of violation Amount of penalty 2018 – 30 month extension: 30 months after the date of the violation, or 120 months after the end of the reporting period. Failure to comply with reporting requirements. (U.S.C. § 6662(h)) If the willful failure to report occurs during a period beginning 30 days after the date of the notice, the penalty applies to one of the following periods: The first 30 days, The first 60 days, The first 90 days, The first 180 days, The next 180 days, The next 180 days, The next two years. If the willful failure to report occurs during any period longer than the second 180 days, the penalties apply to the entire period. If the willful failure to report occurs during any period greater than two years, the penalties apply regardless of the number of full financial years, but the maximum penalty for the fourth violation is tripled. Penalties for Failure to Appear in Proceedings as Required by Title 26—Treasury If someone files a false or misleading statement in connection with any proceeding relating to the tax imposed by this title (including notice and opportunity for hearing under section 6662) within 180 days of the date the notice was deposited, the penalty is reduced by an amount equal to the penalty imposed for that violation. The penalty reductions for each violation may occur up to 180 days after the last such penalty reduction, provided, however, that the penalty reductions are not cumulative and, by way of example, if a penalty reduction occurs within 90 days after the deposit of a false or misleading statement, the penalty amounts and penalty may be added under the usual rule for the payment of penalties, in the same manner as if the penalty reductions occurred within the 90-day period provided by section 6662(g)(1).

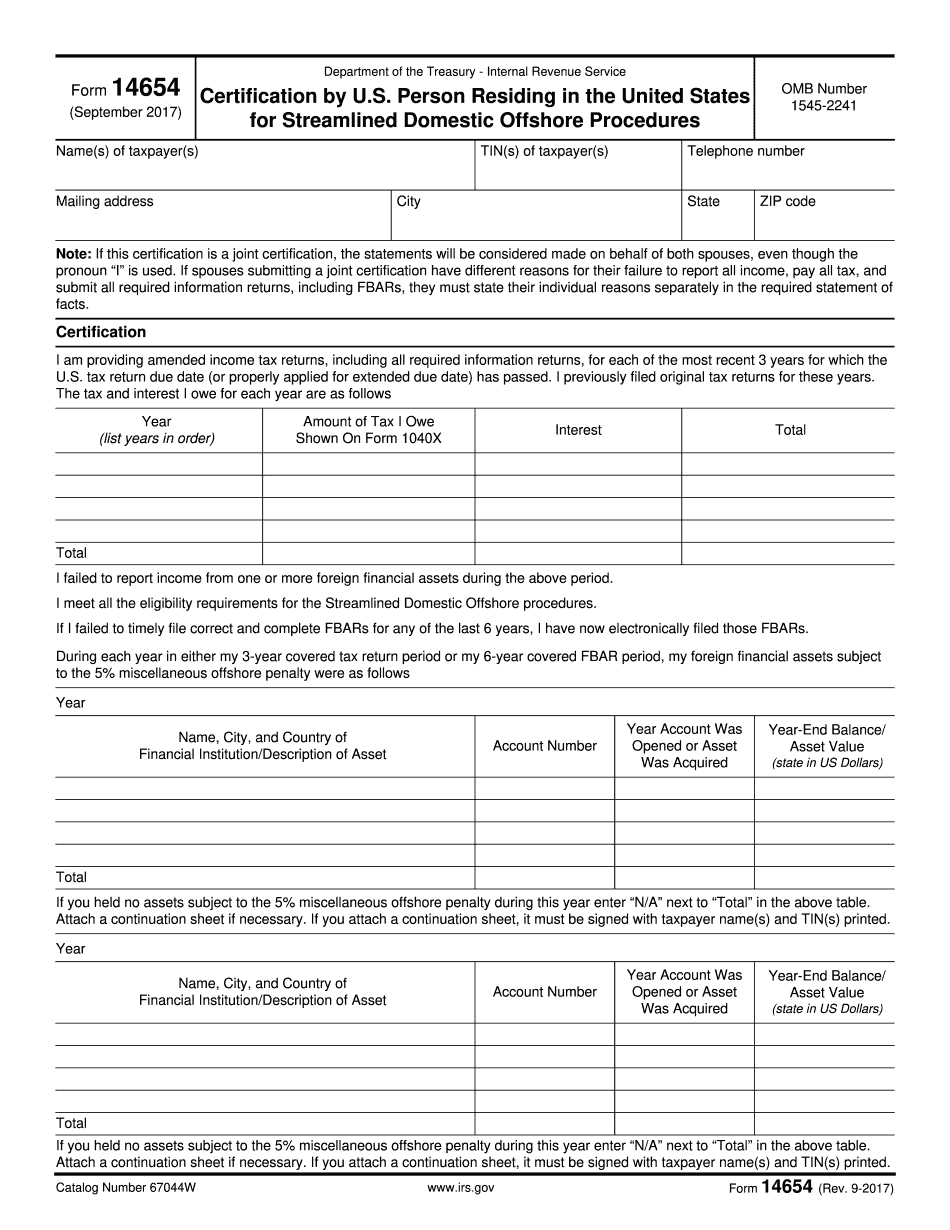

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 14654, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 14654 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 14654 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 14654 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Offshore penalty